MicroStrategy Bitcoin Purchase Adds 487 BTC as Corporate Treasury Strategy Faces 27% Stock Decline

In Brief

MicroStrategy executed a $49.9 million Bitcoin purchase acquiring 487 BTC at an average price of $102,557 per coin, bringing total corporate holdings to 641,692 BTC valued at approximately $47.5 billion.

The acquisition occurred days after Bitcoin slipped below $100,000 in early November, with CEO Michael Saylor maintaining a $150,000 year-end price target despite market turbulence.

MicroStrategy’s average Bitcoin cost basis stands at $74,079 across all holdings, representing unrealized gains even as recent purchases occurred at elevated prices above six figures.

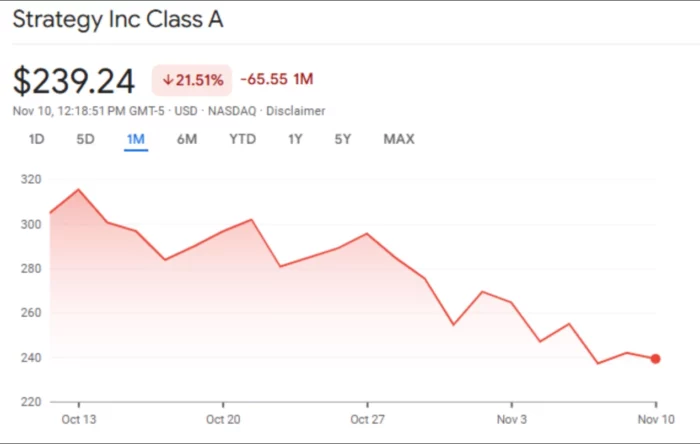

MSTR stock has declined 27% over the past month tracking Bitcoin’s retreat from record highs, intensifying debate about concentration risk in the corporate treasury strategy.

The company raised $770 million through 10% Series A STRE preferred stock issuance targeting institutional investors, with proceeds designated for additional Bitcoin acquisitions and general corporate operations.

MicroStrategy Bitcoin purchase activity continues unabated despite significant market volatility and mounting criticism of the software company’s aggressive cryptocurrency accumulation strategy. The latest 487 BTC acquisition for $49.9 million demonstrates unwavering commitment to the corporate treasury approach that has transformed MicroStrategy from an enterprise analytics firm into the world’s largest corporate Bitcoin holder, even as the strategy subjects shareholders to amplified cryptocurrency price exposure.

Latest Bitcoin Acquisition Expands Holdings Beyond 641,000 BTC

MicroStrategy announced the purchase of 487 BTC for approximately $49.9 million on November 10, representing an average acquisition price of $102,557 per Bitcoin. The transaction increases the company’s total holdings to 641,692 BTC, marking continued expansion of the corporate treasury position that CEO Michael Saylor has pursued since initially pivoting company strategy in August 2020.

The acquisition timing proves notable given Bitcoin’s recent price volatility. The cryptocurrency slipped below $100,000 in early November after maintaining levels above that psychological threshold for six consecutive months. MicroStrategy executed the purchase during this correction period, suggesting the company views temporary price weakness as accumulation opportunity rather than signal to pause buying activity.

Michael Saylor announced the transaction through social media, highlighting the company’s 26.1% year-to-date Bitcoin yield for 2025. This yield metric calculates the appreciation of Bitcoin holdings relative to shares outstanding, providing a measure of how effectively the company’s strategy has delivered Bitcoin exposure to shareholders beyond simple stock price performance.

“Strategy has acquired 487 BTC for ~$49.9 million at ~$102,557 per bitcoin and has achieved BTC Yield of 26.1% YTD 2025. As of 11/9/2025, we hodl 641,692 $BTC acquired for ~$47.54 billion at ~$74,079 per bitcoin.”

The company’s aggregate Bitcoin position carries a total cost basis of approximately $47.54 billion across 641,692 coins, producing an average purchase price of $74,079 per Bitcoin. This cost basis substantially below current market prices provides meaningful unrealized gains on the overall position, even as recent acquisitions occurred at elevated valuations above $100,000 per coin.

Strategy has acquired 487 BTC for ~$49.9 million at ~$102,557 per bitcoin and has achieved BTC Yield of 26.1% YTD 2025. As of 11/9/2025, we hodl 641,692 $BTC acquired for ~$47.54 billion at ~$74,079 per bitcoin. $MSTR $STRC $STRD $STRE $STRF $STRK https://t.co/jTEikuB5RY

— Michael Saylor (@saylor) November 10, 2025

Corporate Treasury Strategy Generates Amplified Volatility Exposure

MicroStrategy’s Bitcoin-focused treasury strategy has fundamentally transformed the company’s risk profile and stock price behavior. MSTR shares now function effectively as a leveraged Bitcoin exposure vehicle, with stock price movements typically exceeding Bitcoin’s percentage changes in both directions due to balance sheet concentration and market perception of execution risk.

The past month demonstrates this amplified volatility dynamic clearly. MSTR stock declined 27% as Bitcoin retreated from recent highs above $108,000 toward the mid-$90,000 range. This outsized stock decline relative to Bitcoin’s more modest percentage correction reflects several factors compounding direct cryptocurrency exposure.

Market participants assess ongoing financing capacity when evaluating MicroStrategy’s stock. The company has funded Bitcoin acquisitions primarily through debt issuance and equity offerings rather than operational cash flow from its legacy software business. Each Bitcoin purchase at elevated prices raises questions about sustainable financing availability if cryptocurrency markets enter extended downturns that limit access to capital markets on favorable terms.

The recent $770 million preferred stock issuance illustrates both the company’s continued capital market access and the cost of maintaining Bitcoin accumulation. The 10% coupon rate on Series A STRE preferred shares represents substantial ongoing capital costs that must be serviced through operational cash flow or additional financing. This fixed obligation creates pressure to generate returns exceeding the financing costs, potentially constraining strategic flexibility if Bitcoin appreciation slows or reverses.

Concentration risk concerns intensify as MicroStrategy’s Bitcoin holdings grow relative to company market capitalization and operational business value. The 641,692 BTC position valued at approximately $47.5 billion dwarfs the company’s legacy enterprise software operations, which generate modest revenue and profitability. This imbalance means Bitcoin price movements overwhelmingly determine shareholder returns, effectively eliminating diversification benefits and operational business considerations from investment thesis.

Saylor Maintains Bullish Conviction Despite Market Correction

Michael Saylor continues projecting confidence in Bitcoin’s trajectory despite the recent price correction below $100,000. The CEO set a $150,000 year-end target for Bitcoin, representing approximately 50% appreciation from current levels within the remaining weeks of 2025. This ambitious projection maintains the bullish stance Saylor has consistently communicated throughout MicroStrategy’s Bitcoin accumulation campaign.

Saylor’s public messaging emphasizes viewing short-term volatility as noise obscuring Bitcoin’s long-term value proposition. The CEO frames price corrections as accumulation opportunities for investors with conviction in Bitcoin’s role as digital property and inflation hedge. This philosophical approach rationalizes continued aggressive buying during market weakness rather than pausing acquisitions to preserve capital or wait for greater price stability.

The $150,000 year-end target implies Saylor expects catalysts to emerge driving significant near-term appreciation. Potential catalysts cited by Bitcoin bulls include increased institutional adoption through spot ETF products, central bank diversification into Bitcoin reserves, escalating monetary debasement concerns, or geopolitical developments driving safe-haven demand. However, the compressed timeline to year-end creates considerable execution risk for reaching such elevated price targets.

Critics characterize Saylor’s continued bullishness as confirmation bias or promotional positioning designed to support MicroStrategy’s capital raising activities. The company benefits from elevated Bitcoin enthusiasm through improved access to equity and debt markets for funding additional acquisitions. Skeptics question whether public price predictions serve informational purposes or function primarily as marketing supporting the company’s financing operations.

Preferred Stock Issuance Demonstrates Ongoing Capital Market Access

The successful $770 million Series A STRE preferred stock offering completed on Friday provides evidence that institutional investors continue supporting MicroStrategy’s Bitcoin acquisition strategy despite market volatility and stock price declines. The 10% coupon rate attracted capital from investors seeking stable income returns while potentially participating in Bitcoin exposure through the preferred shares’ convertibility features.

The preferred stock structure targets institutional investors with different risk-return profiles compared to common equity holders. The 10% annual dividend provides fixed income streams appealing to investors prioritizing yield over growth, while the institutional investor base brings stability compared to retail-dominated common stock trading. This diversified capital structure enables MicroStrategy to access multiple investor segments with varying Bitcoin exposure appetites.

However, the 10% coupon rate represents substantial ongoing costs that constrain operational flexibility. Based on the $770 million issuance size, MicroStrategy committed to approximately $77 million in annual preferred dividend payments. The legacy software business must generate sufficient cash flow to service this obligation alongside existing debt costs from previous convertible note issuances used to fund Bitcoin purchases.

The preferred stock proceeds designated for “further Bitcoin purchases and general corporate operations” maintain ambiguity about specific allocation between cryptocurrency accumulation and operational business needs. This flexibility allows management to adjust Bitcoin buying pace based on market conditions and financing costs while funding ongoing software business requirements. The lack of specific allocation commitments provides operational latitude but reduces transparency for investors evaluating capital deployment efficiency.

Stock Price Correlation to Bitcoin Intensifies Concentration Concerns

The 27% MSTR stock decline over the past month closely tracking Bitcoin’s retreat from record highs demonstrates the complete correlation between MicroStrategy’s equity value and cryptocurrency price movements. This tight relationship validates both supporter and critic perspectives on the corporate treasury strategy, depending on Bitcoin price direction and investment timeframe.

Supporters view the correlation as feature rather than bug, arguing MicroStrategy provides leveraged Bitcoin exposure through a publicly-traded equity vehicle accessible via traditional brokerage accounts and retirement plans. The company effectively functions as a Bitcoin acquisition mechanism for investors unable or unwilling to directly hold cryptocurrency through exchanges or custody solutions. The operational business provides minimal value from this perspective, serving primarily as vehicle for implementing the Bitcoin accumulation strategy.

Critics contend the correlation creates unacceptable concentration risk for equity investors expecting diversified business operations. Traditional software company shareholders who invested before the Bitcoin pivot face unwanted cryptocurrency exposure that has completely transformed the investment thesis. The correlation also amplifies downside risk during crypto bear markets, potentially generating shareholder losses exceeding direct Bitcoin holding losses due to financing costs, forced liquidation risks, or market pessimism about strategy sustainability.

The correlation strength has implications for portfolio construction and risk management. Investors holding both MSTR stock and direct Bitcoin positions gain no diversification benefits, instead concentrating exposure through different instruments. Conversely, investors seeking Bitcoin exposure through equities must accept the additional risks MicroStrategy’s capital structure and operational business introduce compared to direct cryptocurrency ownership or spot Bitcoin ETF products.

Average Cost Basis Provides Valuation Context for Holdings

MicroStrategy’s $74,079 average purchase price across all Bitcoin holdings provides important context for evaluating the position’s financial performance and sustainability under various market scenarios. The cost basis substantially below current prices generates unrealized gains that create financial cushion against moderate price declines while demonstrating the strategy has captured significant appreciation since inception.

The average cost calculation reflects MicroStrategy’s multi-year accumulation campaign beginning in August 2020 when Bitcoin traded below $12,000. Early purchases at dramatically lower prices establish a favorable blended cost basis that subsequent acquisitions at elevated levels gradually increase. This dollar-cost averaging effect across a sustained bull market has produced the current $74,079 average, which remains attractive relative to today’s prices despite recent purchases above $100,000.

However, the rising average cost basis reveals a mathematical inevitability as Bitcoin prices appreciated and acquisition sizes grew. Early purchases represented smaller absolute dollar amounts at lower prices, while recent transactions involve larger capital deployments at higher unit prices. This dynamic means recent acquisitions carry disproportionate weight in determining overall position profitability going forward, even though they represent modest percentages of total coin holdings.

The cost basis provides a theoretical liquidation floor where MicroStrategy could theoretically sell holdings without realizing losses. In practice, forced liquidation scenarios would likely occur at prices well above cost basis due to debt covenants, market volatility, and the impracticality of orderly unwinding such a large position. Nevertheless, the cushion between cost basis and current prices provides some downside protection against scenarios requiring partial position sales to meet obligations.

Bitcoin Yield Metric Attempts to Quantify Strategy Performance

MicroStrategy’s reported 26.1% year-to-date Bitcoin yield for 2025 represents an alternative performance metric designed to measure how effectively the company delivers Bitcoin exposure to shareholders relative to share count dilution. This calculation attempts to separate Bitcoin price appreciation from capital structure effects that impact traditional per-share metrics.

The Bitcoin yield formula divides the change in Bitcoin holdings per share by the Bitcoin holdings per share at period beginning. This approach credits the company for acquiring additional Bitcoin through accretive capital raises while penalizing dilutive financing that increases shares outstanding faster than Bitcoin accumulation. The metric aims to show whether management is efficiently converting capital raises into incremental shareholder Bitcoin exposure.

The 26.1% year-to-date yield suggests MicroStrategy successfully increased Bitcoin holdings per share during 2025 despite multiple capital raises. This performance indicates capital market transactions occurred on terms favorable enough that new Bitcoin acquisitions outpaced share dilution effects. From this perspective, management executed the accumulation strategy efficiently by timing offerings and structuring transactions to maximize shareholder Bitcoin exposure growth.

However, the Bitcoin yield metric faces criticism for obscuring important financial dynamics. The calculation ignores financing costs associated with debt issuances, preferred dividends, and potential common stock dilution from convertible securities. It also doesn’t account for opportunity costs of capital deployed into Bitcoin versus alternative uses including software business investment, debt reduction, or shareholder returns through dividends or buybacks. These omissions limit the metric’s utility for comprehensive strategy evaluation.

Debt Obligations Create Fixed Costs Regardless of Bitcoin Performance

MicroStrategy’s Bitcoin acquisition financing strategy relies heavily on convertible debt instruments and preferred equity carrying fixed payment obligations that create ongoing cash requirements independent of cryptocurrency price performance. These obligations introduce financial risk absent from direct Bitcoin ownership or spot ETF vehicles that don’t employ leverage.

The company has issued multiple series of convertible senior notes with varying maturity dates and interest rates to fund Bitcoin purchases. These instruments require semi-annual interest payments and eventual principal repayment at maturity unless holders convert to common stock based on conversion price terms. The aggregate debt burden represents substantial fixed costs that the legacy software business must generate cash flow to service, creating pressure on operational performance.

The recent 10% preferred stock issuance adds $77 million in annual dividend obligations to the fixed cost structure. Combined with existing convertible debt interest payments, MicroStrategy faces nine-figure annual financing costs that must be covered through operational cash flow or additional capital raises. This fixed cost base creates vulnerability during extended crypto bear markets when raising new capital might prove difficult or expensive.

The convertible debt structure provides some flexibility through conversion features that could eliminate debt obligations if Bitcoin appreciation drives MSTR stock above conversion prices. Bondholders converting to equity would relieve MicroStrategy of repayment obligations while diluting existing shareholders. However, conversion depends on stock price performance, meaning debt obligations persist if Bitcoin and MSTR stock remain depressed through maturity dates.

Regulatory and Accounting Treatment Affects Financial Reporting

MicroStrategy’s Bitcoin holdings receive impairment-only accounting treatment under current US GAAP rules, creating financial statement dynamics that poorly represent economic reality. The company must recognize impairment charges when Bitcoin prices decline below cost basis but cannot mark holdings to market value when prices appreciate, resulting in balance sheet carrying values that substantially understate position value during bull markets.

This accounting treatment creates reported losses during Bitcoin price corrections that don’t reflect economic losses unless the company actually sells at depressed prices. Conversely, unrealized gains during price appreciation remain unrecognized in financial statements until Bitcoin sales occur. The asymmetric treatment distorts traditional financial metrics like book value, earnings, and return on assets that investors typically use for company analysis.

Tax treatment of Bitcoin holdings adds additional complexity. The IRS treats cryptocurrency as property for tax purposes, meaning sales trigger capital gains taxes on appreciated holdings. MicroStrategy’s substantial unrealized gains create large deferred tax liabilities if the company ever needs to liquidate positions. This tax overhang reduces the net proceeds available from asset sales compared to the market value of holdings.

Proposed accounting rule changes would allow digital asset holders to mark positions to fair value each reporting period, eliminating the impairment-only treatment asymmetry. Such changes would more accurately reflect MicroStrategy’s financial position by recognizing unrealized gains and losses, but would also introduce greater income statement volatility as Bitcoin price fluctuations flow directly through earnings each quarter.

Corporate Bitcoin Strategy Influences Broader Institutional Adoption

MicroStrategy’s multi-year Bitcoin accumulation campaign has influenced institutional thinking about cryptocurrency as corporate treasury asset, though few companies have replicated the strategy’s scale or conviction. The company’s experience provides case study data for CFOs and treasurers evaluating Bitcoin allocation decisions, both demonstrating potential benefits and revealing associated risks.

Several smaller public companies have followed MicroStrategy’s lead with modest Bitcoin treasury allocations, including software firms, cryptocurrency-related businesses, and investment vehicles. However, the vast majority of corporate treasuries have declined to hold significant Bitcoin positions, suggesting most finance executives view the volatility and operational complexity as outweighing potential benefits for their organizations.

The strategy’s influence extends beyond direct copycats to broader institutional education about Bitcoin fundamentals and custody solutions. MicroStrategy’s public disclosures, Saylor’s evangelism, and the company’s operational experience have provided learning opportunities for finance professionals researching cryptocurrency. This educational contribution arguably represents meaningful value even for institutions ultimately deciding against Bitcoin allocations.

Critics argue MicroStrategy’s approach represents cautionary tale rather than blueprint for corporate treasury management. The 27% stock decline during Bitcoin’s recent correction demonstrates the volatility consequences of concentrated cryptocurrency exposure. The financing complexity, accounting challenges, and regulatory uncertainties create operational burdens that most companies prefer avoiding even if acknowledging Bitcoin’s long-term potential.

Investment Thesis Depends on Bitcoin Price Trajectory and Timeline

MicroStrategy’s ultimate success or failure as investment vehicle depends almost entirely on Bitcoin’s long-term price trajectory and the timing of appreciation relative to company financing obligations. This simple reality makes MSTR investment thesis inseparable from Bitcoin investment thesis, with company-specific factors playing secondary roles in determining shareholder outcomes.

Bulls argue Bitcoin’s fixed supply, growing institutional adoption, monetary inflation trends, and network effect dynamics support long-term appreciation that will validate MicroStrategy’s aggressive accumulation. From this perspective, short-term volatility and financing costs represent acceptable prices for gaining exposure to an appreciating asset class. The strategy succeeds if Bitcoin reaches levels substantially above current prices within timeframes allowing profitable refinancing of maturing obligations.

Bears contend Bitcoin’s volatility, regulatory risks, technological competition from alternative cryptocurrencies, and potential bubble dynamics create unacceptable downside scenarios for corporate treasury deployment. The financing complexity and fixed obligations introduce additional risks absent from direct Bitcoin ownership, making MicroStrategy inferior to spot Bitcoin or ETF exposure for investors bullish on cryptocurrency. The strategy fails if Bitcoin enters extended bear market or fails to appreciate enough to service accumulated debt and preferred obligations.

The tension between these perspectives creates trading volatility and divergent investor reactions to company announcements. Each Bitcoin purchase generates enthusiasm from bulls viewing it as conviction demonstration while prompting concern from bears seeing increased concentration risk. This dynamic ensures MSTR remains among the most volatile large-cap stocks regardless of broader market conditions.

Market Tests Whether Corporate Bitcoin Model Proves Sustainable

The coming quarters will provide crucial evidence about whether MicroStrategy’s corporate Bitcoin strategy represents sustainable innovation in treasury management or an unsustainable experiment that requires reversal during the next major crypto downturn. Several specific tests will help answer this question.

Capital market access during market stress represents the critical test. If Bitcoin enters sustained bear market with prices declining 50% or more from recent highs, can MicroStrategy still access debt and equity markets on reasonable terms for refinancing maturing obligations and funding operations? The 2022 crypto bear market provided one data point, but the company’s current debt load and elevated Bitcoin cost basis create different dynamics than earlier cycle stages.

Convertible debt conversion outcomes will significantly impact shareholder dilution and financial flexibility. If MSTR stock trades above conversion prices when bonds mature, converting bondholders eliminate debt obligations while diluting equity. If stock trades below conversion prices, MicroStrategy must repay principal through cash generation, asset sales, or refinancing. These different paths produce dramatically different outcomes for common shareholders.

Operational business performance determines the company’s ability to service fixed obligations without additional financing. The legacy software business must generate sufficient cash flow to cover interest payments, preferred dividends, and operational requirements. Deteriorating software business results would force greater reliance on capital markets access, increasing vulnerability to market conditions and financing costs.

Regulatory developments around corporate Bitcoin holdings, cryptocurrency taxation, and accounting treatment will affect the strategy’s attractiveness and operational burden. Favorable regulatory clarity could reduce compliance costs and remove adoption barriers for other companies considering Bitcoin treasury allocations. Restrictive regulations could increase costs or force strategy modifications that reduce efficiency.

Missed buying crypto at the market bottom?

No worries, there's a chance to win in crypto casinos! Practice for free and win cryptocurrency in recommended casinos! Our website wheretospin.com offers not only the best casino reviews but also the opportunity to win big amounts in exciting games.

Join now and start your journey to financial freedom with WhereToSpin!

Middle East

wheretospininkuwait.com provides a comprehensive selection of trusted online casino reviews for the Middle East أفضل كازينو على الإنترنت. The platform features well-established casinos supporting crypto deposits in the region, including Dream Bet, Haz Casino, Emirbet, YYY Casino, and Casinia.

South Africa and New Zealand

In the South African online casino market, wheretospin.co.za highlights top-rated platforms and online casinos such as True Fortune Casino and DuckyLuck. Meanwhile, for New Zealand players, wheretospin.nz showcases highly recommended casinos, including Casinia, Rooster.bet, and Joo Casino.